The Worst Time to Enter India Has Always Been the Best Time to Enter India

Every major crisis in India's last 30 years — 1991, 2013, COVID — was followed by the structural reforms that made the next decade. The companies that entered during the worst moments captured the best structural positions. The ones that waited for stability arrived after the advantage was already built.

In June 1991, India airlifted 47 tonnes of gold to the Bank of England.

Not as a transaction. As collateral. The country had $1.2 billion in foreign exchange reserves — enough to cover 13 days of imports. Moody's had downgraded the sovereign rating. India was days away from defaulting on its international obligations.

If you were a global company evaluating India that month, every rational signal said: wait.

The companies that didn't wait built the positions that defined the next three decades.

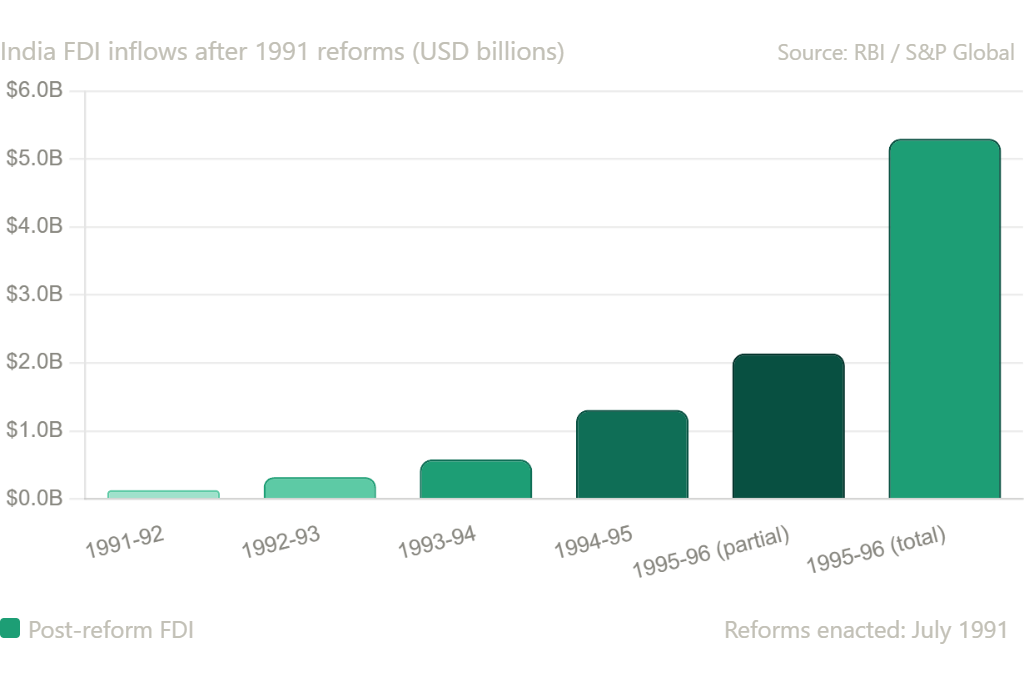

Ford, Samsung, and Coca-Cola entered India by 1993 — right into the wreckage of the crisis, before the economy had stabilised, before anyone knew if the reforms would hold. Foreign investment went from $132 million in 1991-92 to $5.3 billion by 1995-96. The companies that moved in the first two years captured the distribution networks, the partnerships, the talent relationships, and the regulatory knowledge that late entrants had to spend a decade trying to buy.

The ones who waited for stability arrived after the advantage was already built.

This Has Happened Three Times in Thirty Years

The 1991 pattern isn't a one-off. It's a repeating cycle.

The 1991 crisis forced India to dismantle the Licence Raj, open FDI to 100% equity in several sectors, establish SEBI, and create the NSE. These weren't reforms India chose. They were reforms the crisis forced. Every one of them created the conditions for the next decade of growth.

In 2013, India was in what Morgan Stanley called the "Fragile Five." The rupee fell sharply. The current account deficit hit 4.8% of GDP. That crisis produced the Insolvency and Bankruptcy Code, GST, and an inflation targeting framework that held firm during 2022's most brutal global tightening in 40 years.

Then COVID. Supply chains collapsed. India's economy contracted. The government responded with the PLI scheme — Production Linked Incentives — launched in March 2020 across 14 sectors. That scheme, designed precisely because COVID exposed India's manufacturing vulnerability, accelerated a shift that had started in 2014. Mobile manufacturing units went from 2 in 2014-15 to over 300 today, with production value rising 28-fold. In 2024, India overtook China as the top smartphone exporter to the US.

Each crisis. Each set of reforms. Each decade of structural advantage for the companies that were already there.

What Separates India From Every Other Emerging Market

I've done primary research with 237+ companies evaluating India — market entry decisions, GCC setups, manufacturing bets. The conversation that comes up most often is some version of: "We want to wait until things settle down."

That's the wrong frame. And it's a specifically India-wrong frame.

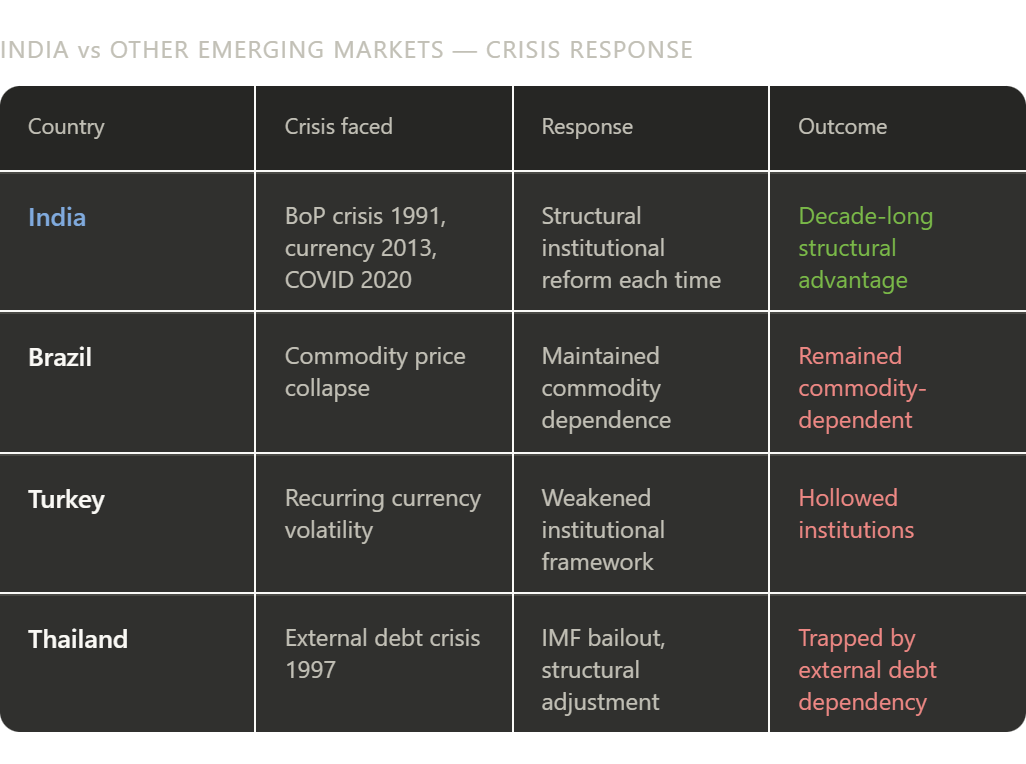

Brazil faced commodity pressure and stayed commodity-dependent. Turkey faced currency volatility and hollowed its institutions. Thailand faced external debt and got trapped by it. None of them executed the crisis-to-reform-to-advantage cycle that India has repeated three times in thirty years.

The reason isn't luck. It's institutional. India reformed when it had no choice — and those forced reforms consistently produced the structural conditions for the next decade.

What's Being Built Right Now

The current pressure is real. Currency volatility, external shocks, tariff uncertainty. I'm not dismissing it.

But the building blocks of the next cycle are already visible. Four semiconductor fabs starting operations this year. Renewable capacity crossing 266 GW — hitting the 500 GW non-fossil target five years ahead of schedule. The SHANTI Act opening nuclear energy to private participation for the first time, targeting 100 GW by 2047. An ₹85,000 crore coal gasification programme converting abundant domestic resources into a potential crude import substitute.

And India is entering all of this at roughly $3,000 per capita — the point where large developing economies typically enter their consumption S-curve. China entered this transition around 2008-2010. What followed was a decade that reshaped global business.

India is entering the same transition now. With $640 billion in macro reserves. With institutional frameworks built through three successive crises.

The companies that entered in 1991 didn't know the Licence Raj would fall. The ones that entered in 2013 didn't know GST was coming. They moved because they understood something simpler: that India converts external pressure into institutional reform, and institutional reform into decade-long structural advantage.

The worst time to enter India has always been the best time to enter India.

The question is whether you're the company that understands that — or the one that reads about it ten years later.

Frequently asked questions

Why is the worst time to enter India often the best time?

India's crises consistently force structural reforms — opening FDI, building regulatory institutions, launching schemes like PLI — that compound into a decade of growth. Companies that arrive during the dislocation capture distribution, talent, and partnerships that late entrants cannot replicate at any price.

Which companies entered India during the 1991 crisis and what happened?

Ford, Samsung, and Coca-Cola all entered by 1993, right after India airlifted 47 tonnes of gold to the Bank of England and reserves covered only 13 days of imports. Foreign investment grew from $132 million in 1991-92 to $5.3 billion by 1995-96, and these early movers captured market positions that defined the next three decades.

How has the PLI scheme changed Indian manufacturing?

The Production Linked Incentive scheme launched in March 2020 across 14 sectors. Mobile manufacturing units grew from 2 in 2014-15 to more than 300 today, with production value rising 28-fold. By 2024 India had overtaken China as the top smartphone exporter to the United States.

Why has India repeatedly turned crises into growth while Brazil, Turkey, and Thailand have not?

The 1991, 2013, and 2020 crises each forced reforms India would not have chosen voluntarily — the Licence Raj dismantling, the Insolvency and Bankruptcy Code, GST, inflation targeting, the PLI scheme. Other emerging markets faced their own crises but did not execute the same crisis-to-reform-to-advantage cycle, often because their institutional response was weaker.

What is the strategic implication for companies evaluating India entry in 2026?

Waiting for stability is the wrong frame in India specifically because structural reforms typically happen during dislocations, not after them. The advantage is captured before conditions look obvious — companies entering during turbulence are positioning for the reforms that the turbulence will force.

Disagree? Push back.

Straight to Ashwin, not public. The sharpest pushback often becomes the next post.

Get Freshwin in your inbox.

New posts the moment they go live. No fluff, no daily emails, no list-rental nonsense. Reply to anything and it lands in my inbox directly.

Double opt-in. Unsubscribe in one click anytime. No third-party trackers in the email.

Work With Ashwin

ResearchFox helps companies set up GCCs, build innovation functions, and design talent strategies in India.

Get in Touch →